Welcome to the fifth and final part of our strategic growth series. Throughout our preceding posts, we’ve discussed various topics, including:

- The rate at which your credit union needs to grow annually just to stay relevant in the CU movement: 9.2%

- How we arrived at this growth rate

- Why your CU needs to grow and the types of growth

- The long-term ‘speed limit’ for growth within your CU, which is Return on Equity or Return on Average Equity (ROAE)

In the final part of our series, we’ll discuss how to grow your credit union at a rate high enough to remain relevant.

How are credit unions addressing this growth mandate? How do you take action that allows you to be part of the group that survives moving forward? Read below for tangible steps your organization can take.

Set Your Objective

Just like any other goal in life, your first step in achieving an objective is to actually set it. As we’ve covered previously, the need to grow your credit union is an essential point of focus. The first step to take action toward this goal is for your board and management team to:

- Adopt this objective (a minimum long-term growth rate of 9.2% or more annually)

- Ensure your organization understands the “why” behind this requirement

- Set strategic goals that align with achieving this level of growth – either organically or through merger/acquisition

Manage Expenses

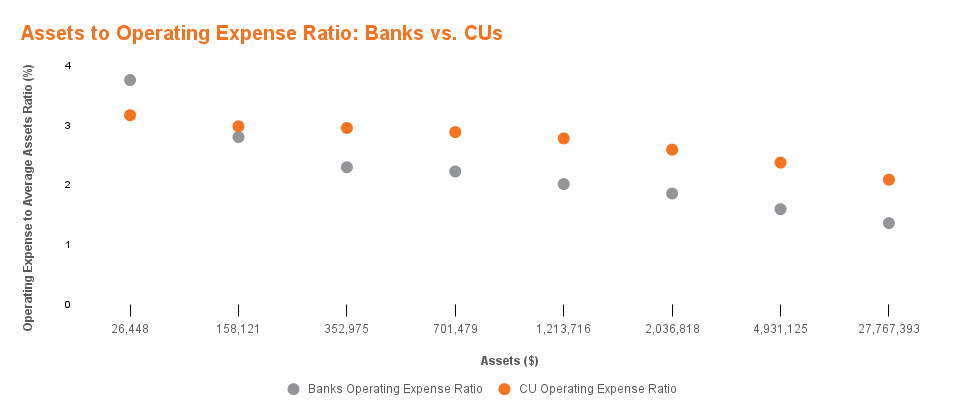

At a basic level, net income is simply the difference of revenue minus expenses. If you were to ask credit union CEOs or industry pundits, almost all would agree that credit unions tend to operate inefficiently. As a general rule, credit unions have higher operating expenses relative to assets.

In the graphic above, you can find where your credit union lies among other banks and credit unions in the marketplace in terms of operative expenses per asset size. Knowing your starting posture is key to measuring improvement as you progress toward your credit union’s goals.

Moving forward with what we’ve learned from this series, operating efficiency has to be an absolute focus of the organization in terms of doing more with less.

Adopt a Productivity Culture

Recent research shows that a highly productive employee will generate approximately 4.8x more value to the enterprise than an employee of average productivity. In other words, you could produce the same value with half the number of employees by using highly productive employees. The pandemic forced credit unions to move quickly to make changes, adopt efficiencies and identify innovative ideas. Productivity was measured as adaptations were implemented. Now is a perfect time for these workplace changes to be evaluated.

One aspect of COVID that has not yet been fully realized is the ability to measure employee productivity in more ways and in more domains than was ever previously possible and use that data to create a productive culture throughout the organization. Credit unions that have already figured this out are racing ahead of the pack. The longer your credit union takes to adopt this mindset, the further behind you’ll fall.

Generate Additional Revenue

When we look at credit unions, a majority are not using all of the tools available to them that could add incremental revenue. In today’s environment, credit unions are no longer able to overlook these tools.

Charitable Donation Accounts (CDAs)

Charitable Donation Accounts, or as we’ve heard it referred to, “The Best Kept Secret in Credit Unions.”

Credit unions give a tremendous amount to charitable organizations and causes. Whether through supporting a cause like the Children’s Miracle Network or a local charity, credit unions give.

Did you know that every year credit unions nationally miss out on 180 million dollars of value because they are not using Charitable Donation Accounts (CDAs)? Hence, why it has been referred to as “the best-kept secret.”

In the past, credit unions didn’t worry about the “cost” of charitable giving – earnings were flush and the amount of giving didn’t seem to meaningfully impact the bottom line.

Today, all of that has changed. As credit unions brace for emerging costs, a more challenging interest rate and economic environment, as well as competition on all fronts, no stone can remain unturned. This is where Charitable Donation Accounts can help solve a major challenge for credit unions.

A CDA would allow a credit union to maintain its current charitable giving while offsetting the expenses credit unions face every day. This is what we like to call the balancing act of staying accountable to members while also finding the best funding avenue for their charitable giving effort.

John Moreno, Managing Partner at Newcleus Credit Union Advisors, explains: “By using the CDA, the credit union can provide current or additional charitable donation value through excess investment returns. In most cases, the credit union is also able to recoup the investment return it would have generated on the funds absent the CDA – so it can truly become a win-win.”

Fintech Partnerships

Credit unions have traditionally not been known to be aggressive, nimble, or on the cutting edge. This can all change by partnering successfully with fintechs entering the marketplace.

While many fintech options are available, special due diligence is needed when partnering in this space to ensure the interests of the fintech and the interests of your members are best served.

A successful partnership can supercharge your ability to grow your loan base, generate additional income streams, and position for future success.

Alternative Investments

Alternative investments available to credit unions can offer substantially higher yields than traditional investments. This added income can help offset traditional benefit expenses.

If a credit union has existing benefit expenses, these investments are able to be a vehicle to generate an additional return, in turn, offsetting those expenses. Given these are often very specialized, a one-size-fits-all approach doesn’t work.

Helping the credit union stakeholders understand the options available, effectively comparing them to one another, and making a prudent choice for the specific credit union is where Newcleus Credit Union Advisors truly shines.

Deferred Compensation Plans

To meet the credit union’s strategic goals and execute on all of these items, you’ll need to ensure you’ve got the right management team, that they’re compensated competitively, and that you can ensure they will be around for the long term.

Setting appropriate goals for your senior management team is key. Newcleus Compensation Advisors has helped many management teams and boards establish key performance indicators, manage compensation and performance incentives, and position compensation around the factors that will drive organizational success.

Once you have the team in place that will carry out these goals, ensuring retention is key, which is done through balancing executive performance, accountability, and the risks/rewards of various plan designs. Comparison and measurement of the risk/reward aspect is key to what sets Newcleus Credit Union Advisors apart from the marketplace.

To Recap

- Your credit union needs a growth expectation as one of your key performance indicators (KPIs). This growth can be organic or inorganic, but long-term, organic growth is going to have to be sustainable at 9.2% or higher to remain relevant.

- There are two key components to improving ROAE: expenses and revenue. On the expense side, credit unions that are thinking outside of the box, compensate higher and create environments where employees can be highly productive. They are able to effectively do more with less. On the revenue side, your CU simply doesn’t have the luxury of doing things inefficiently anymore. You can’t sit on cash waiting for things to happen. If there’s an opportunity to do something more efficiently and safely (i.e. CDAs), you need to be exploring that.

- Lastly, use properly designed compensation and deferred compensation plans to retain the key executives who are going to lead this effort forward. Deferred compensation is key to preventing drag that occurs when there’s turnover. Great compensation plans will hold executives accountable for these growth objectives.

An inspired workforce is a productive one. At Newcleus Credit Union Advisors, we help our client credit unions adapt to this mindset by using corporate social responsibility, charitable donation accounts, online resources, and compensation options to build sustainable growth and a workforce for the future.

For those who are interested in learning more about strategic growth, visit parts one through four of our series, linked below:

Part One: Do You Have Over 9.2% Sustainable Growth Baked into Your Credit Union’s Strategic Plan?

Part Two: A Simple Math Lesson: How Did We Get 9.2% as a Sustainable Growth Rate?

Part Three: Why Does Your Credit Union Need to Grow?

Part Four: What is My CU’s “Speed Limit” for Growth?