Congratulations! You’ve made it through one of the most challenging periods on record! This past year has brought a myriad of unforeseen challenges to credit unions—remote work, loan forbearance, PPP small business loans, a flood of stimulus deposits, loan roll-offs, the list goes on.

But now, as the global pandemic changes gears, it’s important to pivot from an emergency management focus. Here are some ideas to help credit union executives ensure board members are supportive of realistic growth going forward.

The Basics of Credit Union Growth

Credit unions are member-owned financial cooperatives. This means you participate in a virtuous circle where member-owners are also the customers of the organization. This also means that credit unions have relatively limited ways to raise capital to sustain that growth. To help your board with this concept, here is an overview of capital:

Capital is the sum of retained earnings that have been reserved to cushion for anticipated and unidentified losses. Capital also acts as a base for future growth. Finally, capital provides a means to meet competitive pressures as they arise.*

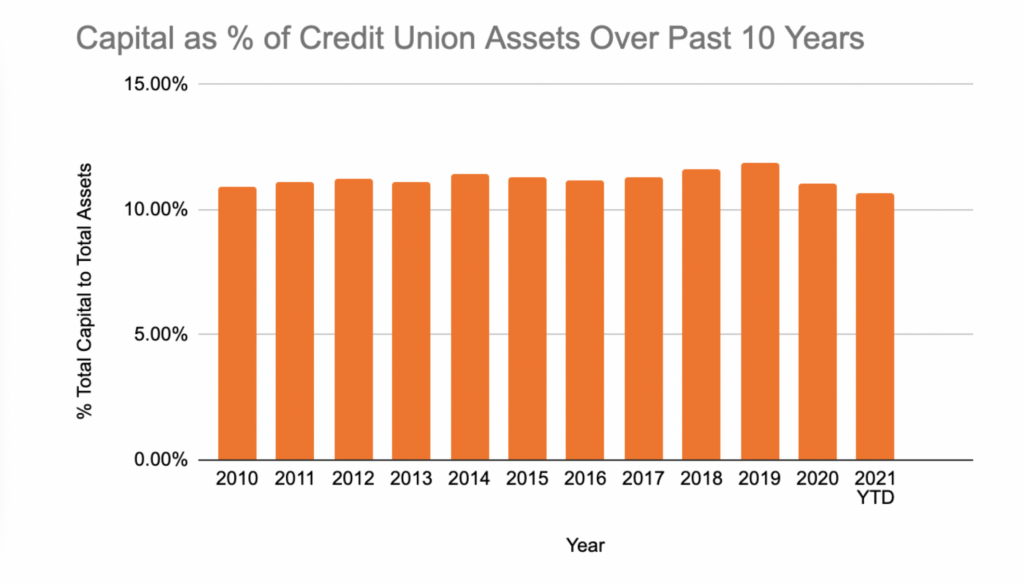

Since capital acts as a cushion for the risk a credit union takes during normal operations, adequate capital relative to the size of the credit union is essential. As of June 30, 2021, the average percentage of capital to credit union assets across the CU industry was 10.7%. This means that for every $10 held in credit union assets, $1.07 was held as capital.

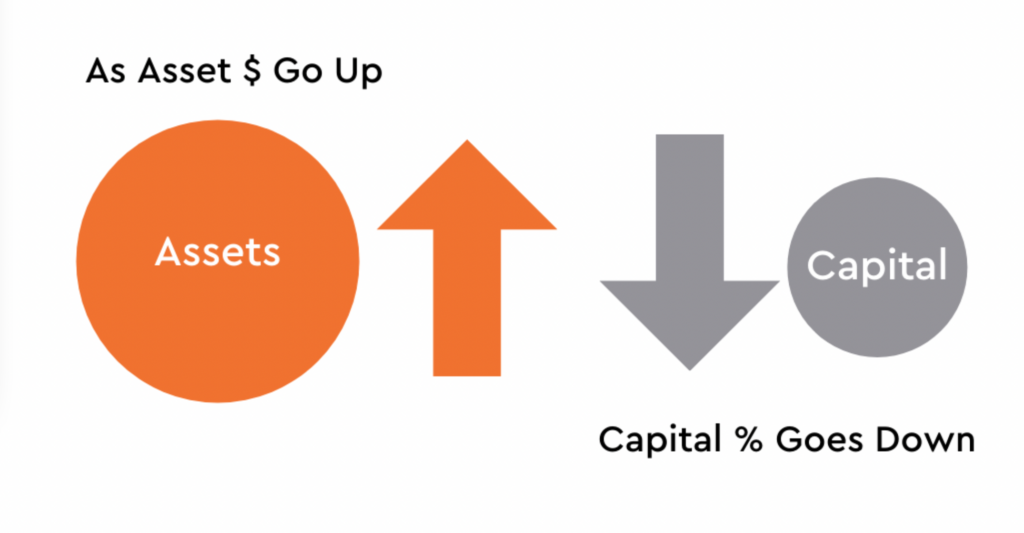

Since capital (and its cousin “Net Worth”) are referenced as a percentage of credit union assets, we can see the impact of the flood of stimulus deposits over the COVID pandemic. If we look to 2019 year-end, industry-wide capital was at 11.9%, and industry assets stood at $1.595 trillion. Fast forward to June 2021, and industry assets are at $2.034 trillion and capital has decreased to 10.7%.

This trend illustrates a VERY important part of the capital equation: If assets go up faster than a certain rate, capital decreases as a percentage of assets. Of course, to be considered solvent, your credit union must maintain a sound capital ratio. The question begs, what is that “certain rate” at which capital decreases as a percentage of assets? First and foremost, board members must understand that credit unions have a rate at which they can sustainably grow and a rate at which they need to sustainably grow.

What you ask is, is this “magical” rate at which your credit union needs to plan to grow to remain relevant?

The simple answer is at or over 9.2% growth per year for the foreseeable future.

If you don’t have a plan to achieve this, it is time to get to work. In this series, we’re going to cover the following key points and questions:

- Do you have over 9.2% sustainable growth baked into your credit union’s strategic plan?

- Why does your CU need to grow?

- Why 9.2% or more as a sustainable growth rate – how was this figure arrived upon?

- How fast can my credit union sustainably grow? What limits/enables your credit union to sustainably achieve this rate of growth?

- What steps can you take to achieve this goal – how are credit unions addressing this growth mandate?