Loan regime split dollar, also known as collateral assignment split dollar, has become a very popular deferred compensation arrangement for credit unions and nonprofit executives.

When structured appropriately split-dollar plans are relatively flexible and have advantages from a taxation and booking standpoint. A properly managed plan may allow for modifications that support your credit union and executive’s needs.

In previous years, however, the financial environment has brought about lower interest rates. Because of this, traditional life insurance policies’ dividend rates have declined.

Let’s talk about the rates on your CEO executive’s split-dollar loan plans—should you lower them?

Looking to The Future

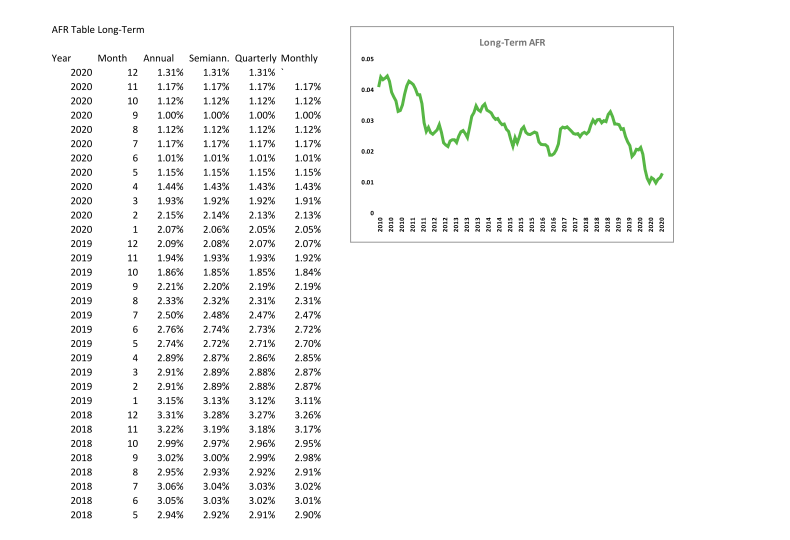

Again, traditional life insurance policies’ dividend rates have declined over previous years. As we look to the future, we forecast this trend may continue. The low rate environment we’ve observed has caused the AFR (applicable federal rate) to decline as well.

The AFR is the minimum interest rate that the IRS allows for private loans. In December 2020, the AFR sat at 1.31%.

As a result of lower policy dividend expectations and the lowered AFR, many credit unions are considering lowering the rate of interest on the loan component of their loan regime split-dollar plans.

As a key stakeholder at your credit union, what should you consider when reviewing this type of adjustment? Let’s discuss.

What is a Split-Dollar Deferred Compensation Plan?

In short, a split-dollar plan is an agreement between two parties to split the cost and benefit of the life insurance premiums, cash values and death benefits.

The split-dollar plans we’ll speak about today are the most popular type currently used in credit unions—and are known as either loan regime split-dollar or collateral assignment split-dollar plans.

There is also a type of split-dollar called equity regime or endorsement split-dollar, which may potentially add to the confusion, but those are quite different and we’ll address those in a future article.

More on Loan Regime and Collateral Assignment Plans

Under a collateral assignment split-dollar life insurance arrangements (CASD), the key executive is the owner and insured of the life insurance policy.

In this policy, the role of the business is to pay premiums using a loan, or series of loans, to the executive to pay premiums due on the policy. On the business’ balance sheet, it’s looked at as a long-term asset and is normally classified as a loan.

With collateral assignment arrangements, the beneficiary is split between the business recovering repayment of the loan, plus any accrued interest on the loan and the executive’s beneficiary.

This is secured by a collateral assignment using forms provided by the carrier or a duly qualified attorney. The collateral assignment protects the credit union from improper action by the executive.

A key aspect of most plans in force today is the repayment of the loan from death benefit proceeds; meaning, the plan will persist until the death of the executive. For reference, according to the Society of Actuaries, a 65-year-old male in 2019 is expected to live to age 85 on average while a female is expected to live to age 87.

Historically, the loans made to finance the purchase of the policy have taken different forms depending on the prevailing rate environment.

Term Loan Arrangements

Currently, the most common structure is a term loan arrangement.

The term loan structure involves the credit union making a single loan for the entire amount of premiums due to the policy. This loan can bear interest or not bear interest.

Commonly, the rate of interest is set at the minimum required rate under section 7872 to avoid income taxation. This rate is the Applicable Federal Rate and is declared through ongoing revenue rulings throughout the year.

The rate of interest charged on the loan to satisfy this requirement is not set in stone. This is the crux of the current push to refinance existing loans for the plan at lower current rates.

What to Consider When Adjusting the Interest Rate of Your CU’s Split-Dollar Agreements

This analysis requires consideration of both qualitative and quantitative factors.

Qualitative Points of Consideration

From the qualitative standpoint, the plan objective and goal of the board with regard to the plan must be reviewed.

- Was this plan structured in order to provide a benefit target regardless of policy performance, or was the benefit target known to be at risk based on other negotiated benefits to the executive?

- Is the board obligated to adjust the plan based on its philosophy or other norms?

- Will the same approach be used for other executive participants in a similar plan? Will the same accommodation be expected to continue after the executive has separated from the credit union?

Remember, the plan ends at the executive’s death.

Quantitative Points of Consideration

Quantitatively, what is the cost to the credit union of making such a change?

- Is there a way to recover a portion of the income expected by the credit union if rates change direction between now and the end of the plan?

- What is the present value of such an adjustment (i.e. the value today of sums to be paid in the future)?

- What further changes may be warranted if policy performance is challenged?

Finally, what is the best, worst and expected case scenario given what we know today?

Seek Out an Experienced Professional

Obtaining that information and reviewing it with a knowledgeable nonconflicted party is key to both making the right decision for the credit union and executing your fiduciary duty as a board member.

With a decrease in long-term interest rates, it might seem like a favorable time to consider restructuring your collateral assignment split-dollar plans. This choice, when executed properly, can help improve your executive’s benefit.

What Other Alternatives Might You Consider?

Other alternatives you might consider under advisement may involve augmenting the current plan with a secondary plan that is different in form. For example, balancing a 457(f) arrangement with the CASD arrangement.

Additionally, for larger plans on higher compensated executives, you may consider further diversifying. To further spread the risk of any one plan design derailing the benefit to the executive, this can be done by using a combination of:

- Traditional (whole) life

- Indexed universal life

- 457(f)

At Newcleus Credit Union Advisors, we have deep experience modeling the contingencies of all plan types. We have worked with both credit unions and their legal counsel to develop innovative solutions to the concerns outlined above. We would be delighted to discuss your situation and see how we might help you. Contact us today.

Interested in learning more about split-dollar plans? Read on in our article “The Truth About Split-Dollar Arrangements.”