A lifetime income non-qualified solution, more commonly referred to as LINQS+, is Newcleus’ proprietary innovation to the traditional supplemental executive retirement plan (SERP) product; which is a form of deferred compensation. The fact that LINQS+ is proprietary is likely why you may not have ever heard of it.

This proprietary innovation to the traditional SERP combines the best of a traditional SERP with a mechanism to enhance executive retention and reduce the cost of the benefits for a financial institution, all while remaining a lifetime benefit.

Today, we have Rachel Wentz, VP and Account Executive at Newcleus, giving a high-level introduction to LINQS+.

Here’s what she has to say.

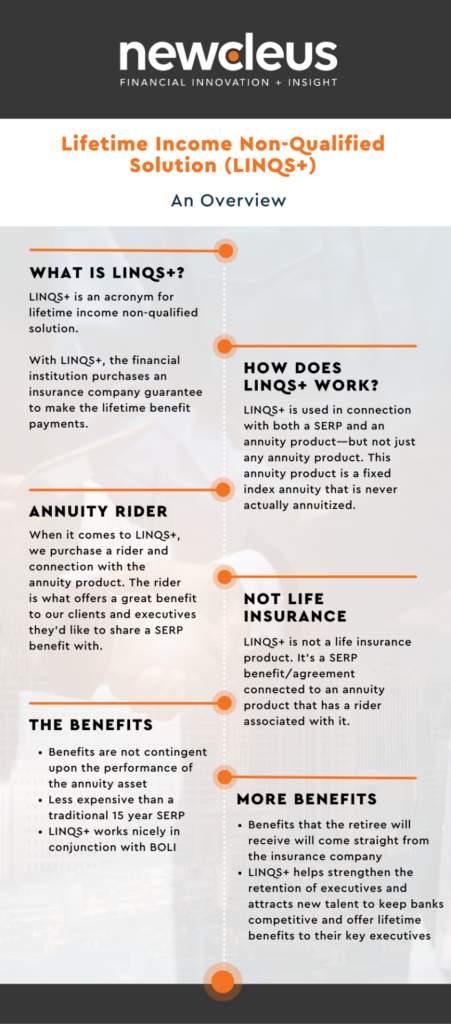

What is LINQS+?

LINQS+ is an acronym for lifetime income non-qualified solution.

It’s a strategy that was developed by our company’s own Flynt Gallagher, President of the Compensation Advisors branch of Newcleus.

With LINQS+, the financial institution purchases an insurance company guarantee to make the lifetime benefit payments. The insurance company takes the longevity, investment, and interest rate risk while the financial institution carries the asset as an investment on the balance sheet and earns interest at current market rates.

How Does LINQS+ Work?

LINQS+ is used in connection with both a SERP and an annuity product—but not just any annuity product. This annuity product is a fixed index annuity that is never actually annuitized.

And there’s a reason behind that.

Annuity Rider

When it comes to LINQS+, our team purchases a rider and connection with the annuity product.

An annuity rider is defined as “a provision you can add to your annuity contract to ensure it meets your financial needs. The main categories of annuity income riders are guaranteed minimum living benefits and guaranteed minimum death benefits.”

The rider, in our case, is what offers a great benefit to our clients and the executives that they’d like to share a SERP benefit with.

And so what is this rider? The rider that’s purchased in connection with the annuity is generally known as a ‘guaranteed minimum withdrawal benefit rider (GMWB),’ which offers a fixed benefit for the life of the annuitant.

A nice feature about annuity contracts is that there’s no medical underwriting required. Typically, in a life insurance contract, if you’re ensuring an individual, you have to go through a full underwriting medical analysis. With annuities, however, you can provide an annuity to one person without underwriting.

A final note, LINQS+ is not a life insurance product. It’s a SERP benefit/agreement connected to an annuity product that has a rider associated with it.

Who Is Involved?

The annuitant is the executive that is offered the SERP benefit.

The bank, credit union, or company will be the owner and beneficiary of the contract.

LINQS+: The Benefits

Benefits are not contingent upon the performance of the annuity asset but are actually guaranteed through the rider.

What does this mean? Simply put, no matter how the asset performs on the annuity contract, the lifetime benefit payment is guaranteed.

This is really important because there are many traditional SERP products, benefit plan arrangements, and retirement plans that are based on the performance of the asset that is purchased in connection with the product.

Secondly, LINQS+ is less expensive than a traditional 15 year SERP. This benefit will also be paid to you for life at the exact amount that was promised.

Additionally, LINQS+ works nicely in conjunction with BOLI, which can be purchased simultaneously to continue to help fund and hedge the benefit and the liability obligation associated with these products.

The benefit obligation is matched dollar for dollar from the liquidity provided by the GMWB rider. This means that the benefits that the retiree will receive will come straight from the insurance company. A check will be issued from them and paid for life.

A final benefit of purchasing LINQS+ is an increase in executive retention that comes with a guaranteed lifetime benefit. It helps strengthen the retention of executives and attract new talent to keep banks competitive and offer lifetime benefits to their key executives.

LINQS+: Real-Life Example

- An executive is to receive $100K annually for 15 years under a traditional SERP; the cost of the plan is $1,500,000 (100K x 15).

- With LINQS+, an investment of $800K will provide a GUARANTEED lifetime benefit stream of the same $100K annually.

- The financial impact is a positive savings of $700K for the financial institution, and the executive receives an enhanced LIFETIME benefit, of at least $2,100,000 based on expected mortality.

Want to learn more about the products we offer at Newcleus? View one of our most recent videos explaining bank-owned life insurance (BOLI), as spoken by Brian McCracken, VP and Account Executive Director at Newcleus.

Or, read on for more frequently asked questions about LINQS+.