At Newcleus CU Advisors, we’ve seen credit unions struggle under the weight deposits inflated by unprecedented government stimulus. As wave 2 of stimulus hit balance sheets in March, credit unions continue to struggle to find ways to deploy excess deposits. With tax refund season right around the corner, you should only expect deposit activity to persist. Some credit unions are using this flow to explore additional investment opportunities they didn’t have the liquidity to pursue – read further to learn more.

Where is the excess liquidity coming from?

Stimulus payments and tax refunds compounded with increased savings have dramatically increased liquidity in the credit union system. Not only have members been saving these stimulus payments, but they have also been paying down their debt, and spending less overall, exacerbating the balance sheet stress felt by credit unions and compressing typical credit union income sources. Additionally, consumer discretionary spending is at a low point, and concerns about underlying economic strength persist. Decreased spending, lower than normal real-estate inventory, and supply-constrained limits on larger-ticket items have further caused new loan applications to slow.

While all of the safety measures and aid packages have been helpful for members as they struggle through the pandemic, they are causing distress to credit unions by swelling balance sheets without generating the needed earnings to maintain this posture. This situation isn’t helped by extremely low rates on investments normally used by credit unions. All of these factors have depressed net worth ratios, led to decreased non-interest income, and have led to credit unions exploring multiple opportunities for investments they haven’t considered before.

701.19 or 721 Investments in the spotlight

Given the expansion of liquidity and limited opportunity for income generation through traditional channels, many credit unions are exploring the use of investment authority under sections 701.19 or 721 of the Federal Credit Union Act. States may have parity with this act or have their own specific regulations. The powers are also called Benefit Funding Offset accounts, Charitable Donation Accounts, or Pre-Funding Accounts. We’ll explain more below:

Under section 701.19, a credit union can invest to offset benefit expenses using investment types not normally permissible for the CU to use. Additionally, section 721 of the act allows similar authority but for the purpose of funding charitable giving. Given current yields and return levels, both of these strategies have the opportunity to provide much-needed additional income to the credit union that chooses to use them.

Below are the approaches used in today’s marketplace to achieve the higher potential return opportunity presented by these sections of the Federal CU Act.

Traditional or “Pure” Investment Strategies

These are investment approaches where the credit union would either directly purchase investments used for the charitable or benefit offset or, utilize the services of an investment manager to build and oversee an investment portfolio. Given the investments that can be used in these programs are much broader than typical CU investments, many CUs using this approach choose to work with a professional investment adviser.

This approach is highly transparent and should have a competitive fee structure. Credit unions using this approach could realize a significant return relative to typical CU investments, however, all volatility goes through the income statement. This can present challenges during times of large downward swings in the market – like March of 2020. The risk of these investments is managed primarily through asset allocation with other factors utilized depending on the manager.

Principal Protected Notes and/or Certificates

These investment options offer a relatively low-risk, investment for credit unions that strive to invest in the markets but don’t want the risk to the principal that comes with investing in the market. With principal-protected notes and certificates, the principal of the investment can have protection embedded in the terms of the note/certificate. There are a tremendous number of this type of program which makes detailed due diligence key when using for the offset and charitable donation options outlined above.

General Account or Indexed CUOLI

General account insurance offers a relatively stable yield profile and a relatively low-risk structure depending on the rating of the carrier. This approach generally offers a steady yet constructive return on the investment. Another form of General Account CUOLI is Indexed CUOLI. Indexed CUOLI uses a reference to an index to calculate the return provided under the policy. This is normally used to offer the potential for an upside return to the purchasing credit union without exposing the CU to volatility or heavy losses.

Customized Strategies

If your credit union is large enough to benefit from customized strategies, alternative options that are offered on a restricted basis or through private placement may be an option that better suits the organization. These highly customized options are generally more complex, and are available to institutional accredited investors, with initial minimum commitments that may range from $10 million and up.

CDAs

Many credit unions are deploying excess liquidity into CDAs. The primary purpose of a CDA is to generate funds to donate to tax-exempt charities chosen by your credit union. This can include the credit union’s own foundation if it has established one under section 501(c)3. Donations made by the CU using a CDA can be offset by the growth of the CDA. Additionally, the credit union (under federal regulation) is permitted to retain up to 49% of the yield on the program, thus this could be additive to the bottom line in addition to helping support your community. This approach can use the investment tools referenced above and is a great way to help your community while also helping your bottom line!

Keep an eye out for an upcoming webinar related to your credit union’s options with all the excess liquidity on your balance sheet.

Read more about how your peer credit unions have been affected by the global pandemic, and how, even in the face of lower yields, they are finding ways to help their members in need in the article below.

Not for profit, not for charity, but for service. The mission of every credit union is to help its members. The current pandemic is the perfect time to use all of your resources to find ways to help members in need. See the example below of a credit union that added $1,000 in credit to each of their members’ credit lines despite reduced spending just in case it was needed! The goodwill you generate by actively seeking to help your members will yield huge dividends even when traditional investments are not.

Read more from the article by William Hunt: How Are Credit Unions Using Excess Liquidity? | Credit Unions https://www.creditunions.com/blogs/industry-insights/how-are-credit-unions-using-excess-liquidity/#ixzz6h0058XCG

How Are Credit Unions Using Excess Liquidity?

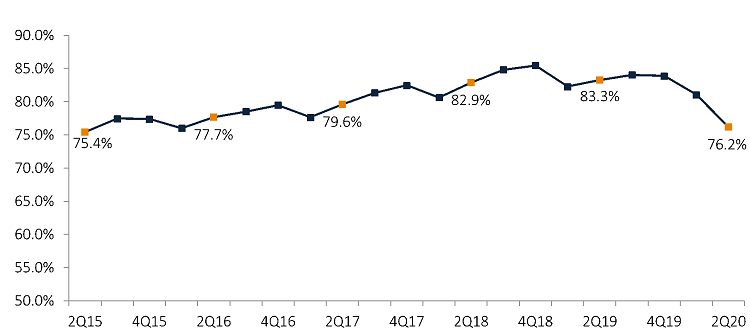

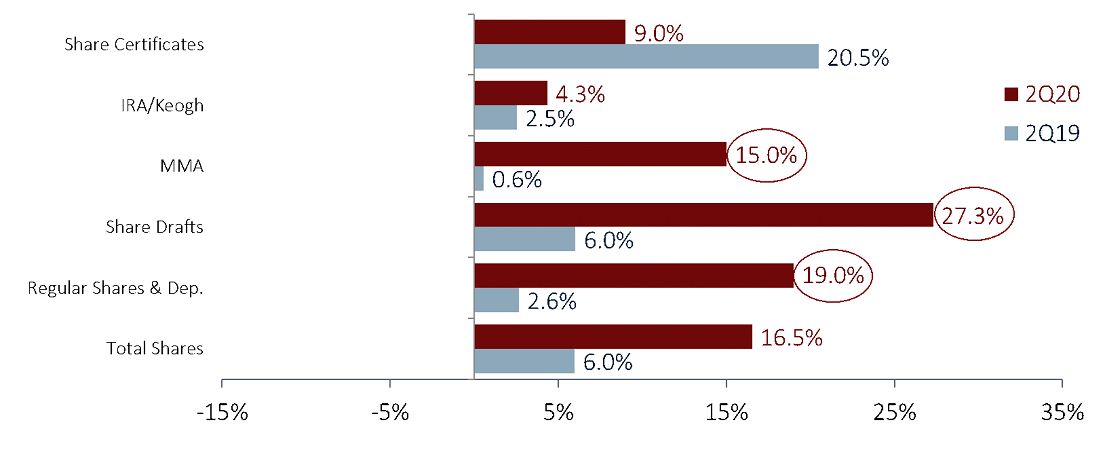

Share balances at U.S. credit unions have grown at near-record rates since the onset of COVID-19 and the resulting lockdowns. According to second-quarter data from Callahan & Associates — representing 99.6% of industry assets — deposit balances at credit unions increased 16.5% year-over-year. This is the fastest annual rate since 2003. Meanwhile, total loan balances rose 6.6%. Together, these top-level dynamics have driven down the industry’s loan-to-share ratio to 76.2% — the lowest level since the first quarter of 2016.

LOAN-TO-SHARE RATIO

The industry’s loan-to-share ratio usually increases between March and June, but heavy share growth has prolonged what is usually a seasonal decline.

The Impact Of COVID-19 On Liquidity

In mid-March, when the uncertainty surrounding COVID-19 was near its peak, it didn’t seem likely the industry would report substantial balance sheet growth during the coming months. However, federal relief programs, a dovish Fed monetary policy, and lenient loan forbearance programs all have aided the U.S. economy. Funds from personal aid checks and increased unemployment have flooded into deposit accounts, and many workers are still earning income while working from home.

Additionally, quarantines and small-business closures have dramatically reduced consumer spending. Consumer originations were down 0.2% year-to-date from June 30, 2019, and overall credit card balances were down 2.4% annually, the first outright decline since 2003. Historically low-interest rates did drive a 94.1% year-over-year increase in first mortgage originations, which, in turn, helped prop up overall loan growth, mainly via refinances.

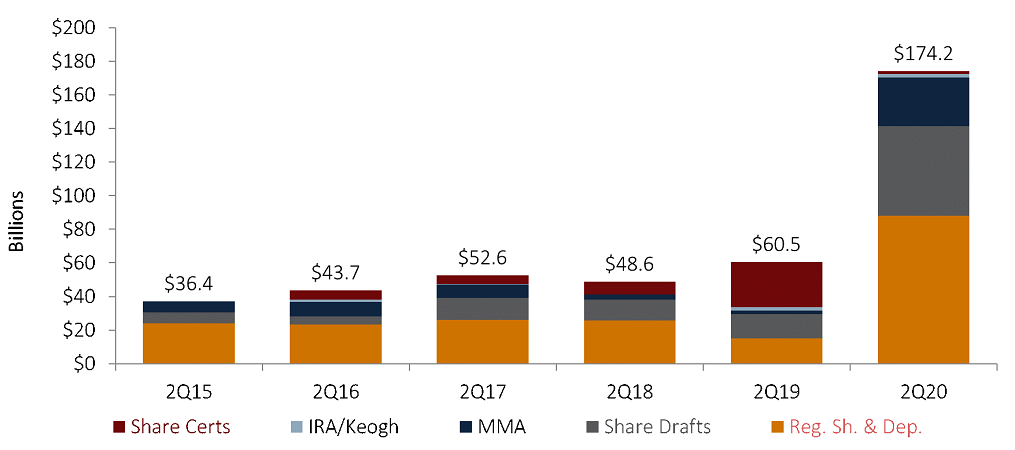

However, stimulus income combined with slowed consumer spending left a lot of new money sitting in deposit accounts. Share drafts and regular shares were up 27.3% and 19.0%, respectively, as of June 30. These are the highest rates for both categories in more than 15 years.

In today’s environment of increased deposit balances and low-interest rates, credit unions have favored holding unlent funds in accessible-cash versus investing in options such as Treasuries and their historically low yields. All told, cash and equivalents balances were up 78.6% annually as of June 30, effectively alleviating the liquidity concerns that were widespread in the second half of 2019.

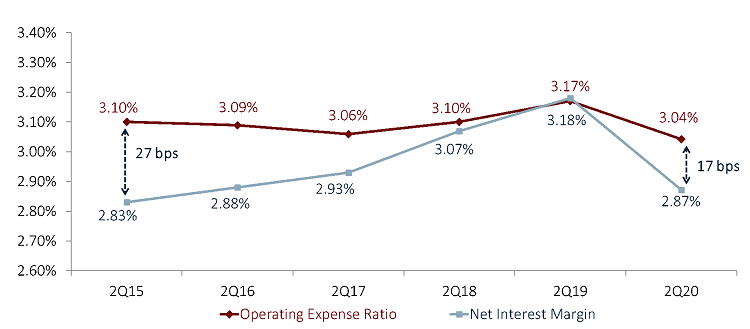

Spread compression and a corresponding decline in net income have replaced last year’s liquidity fears. Sudden rate cuts drove the industry’s net interest margin down 31 basis points to 2.87%, the largest 12-month decline of this century. Year-to-date income from investments, hindered by the low-yielding cash balances, fell 20.4% annually, significantly impacting credit union earnings. As a result, credit union net income totals declined 34.8% year-over-year. This combined with the increase in investment asset balances drove the industry’s net worth ratio down to 10.5%, 92 basis points below the decade-long high reported this past December. Since last quarter, 80 credit unions fell below the NCUA’s well-capitalized ratio of 7%.

In the second quarter of 2019, the net interest margin overtook the operating expense ratio, meaning credit unions could cover day-to-day expenses using only interest income. Thanks to spread compression, that is no longer the case.

Loan Forbearance And Asset Quality

A review of credit union income statements does detract from the more optimistic balance sheet results; however, these top-level metrics underscore many positive trends, namely that credit unions are supporting their members during this pandemic.

All told, the industry’s net income was down $2.5 billion annually, to $4.7 billion year-to-date. However, much of this decline can be attributed to a 51.7% increase in the provision for loan loss. With a year-to-date total of $4.9 billion, the industry’s total provision expense was up $1.7 billion versus last year and accounted for 65.9% of the total decline in net income.

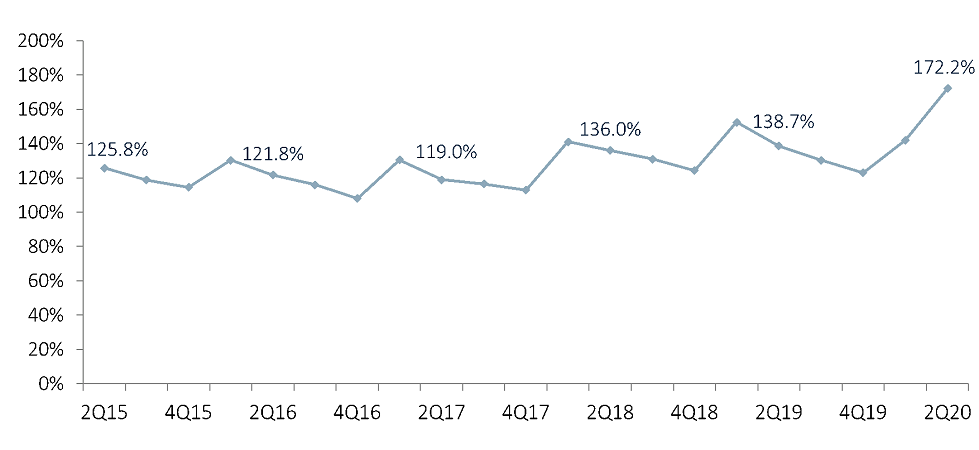

In short, income streams are not performing as poorly as they might seem. Instead, credit unions are strategically repurposing income to help members in need. The increase in provision expense has pushed the industry’s allowance for loan and lease losses up 21.4% annually to $11.5 billion, the highest level on record. With total delinquent loans actually down 2.2%, the nationwide coverage ratio — the amount of allowance for every dollar of delinquent loans — increased to the highest it has ever been, 172.2%.

It is important to examine loan delinquency and the reason behind its decline. Certainly, government stimulus and increased unemployment benefits have played a crucial role in keeping delinquency and charge-offs down. However, relaxed loan forbearance policies at credit unions across the country also have been a major factor.

Spurred by government incentives under the CARES Act, as well as an obligation to the credit union mission of member support, cooperatives have deferred payment on billions of dollars of loans, providing members with some peace of mind during this difficult time. Although credit unions are preparing for these deferred loans to come due, the goodwill generated from these policies could prove invaluable toward ongoing member engagement.

Increasing Member Access To Credit

Credit unions aren’t just setting aside money to cover potential future losses; they also are deploying capital in other ways to benefit their members. For example, many are increasing lines of credit as well as reducing fees — which were down 9.7% annually.

Although loan balances for revolving credit cards fell 2.4% year-over-year, the total amount available grew 8.4%. To give members in need access to quick cash, Wright-Patt Credit Union ($5.7B, Beavercreek, OH), added $1,000 of credit to every member’s credit card line. Other credit unions have applied similar generous policies.

Although many members are using their credit cards less, there is a segment of members desperate for extra credit and many others might need it in the near future.

Not all credit unions are willing to extend this additional unsecured credit, opting instead to hold these riskier loans at their current level. This consideration is important to acknowledge, as a potential surge in delinquencies could leave credit unions overextended, even with a substantial allowance for loan loss. However, the industry is expanding lines of credit in other ways, too.

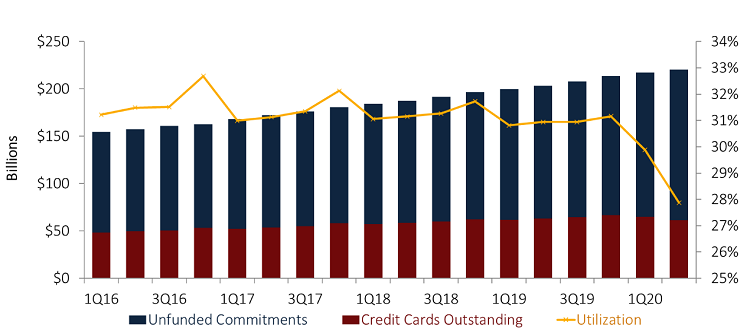

Total revolving open-end real estate LOCs — most often HELOCs — were up 3.6% annually despite a 2.3% annual decline in draws. Overall, unfunded commitments for all loan types at credit unions across the country have increased 11.6% year-over-year. Some of this growth can be attributed to a decline in spending and utilization, but additional access to credit also is a significant part of the equation. The overall surge in deposit balances and decline in spending shows not all members need this additional access to cash. However, some members do and countless others might soon, especially if aid and welfare programs slow down or disappear.

The Bottom Line

Safety measures and aid packages introduced to combat COVID-19 have resulted in liquidity across the credit union industry reaching potentially unwanted levels. However, a combination of increased credit lines, low-interest rates, and a more optimistic outlook for economic reopening should incentivize future spending and help credit unions recover from current net worth pressures.

The delinquency rate deserves close monitoring during the next few quarters, but many institutions have the allowance balances available to cover even a significant increase in loan losses. It will be a tightrope to walk in these uncertain times, but if credit unions can keep deploying excess liquidity to support members while covering their downside risk, the movement will come out of the pandemic having garnered significant goodwill from a membership in need.