GROUP TERM PLANS AND THE FEAR OF RESPONSIBILITIES, TIME, and….UNDERWRITING

by Richard Pearson, Newcleus COO

The following is only one strategy of many offered at Newcleus, but we find the plan type, general need, and context may be the most relatable for employers, employees, or both if you’re responsible for employer-sponsored plans of your organization. The strategy attempts to illustrate the shortcomings of traditional employer-sponsored group term plans, ways to enhance coverage while saving money for both the employer and employee and promote employee retention. You can jump right to the analysis by scrolling below to the Analysis subheading or read on to learn more about turning stressors into opportunities.

In my high school Speech class, we had to prepare an eight-minute-plus original oratory where a portion of my grade was dependent upon student feedback. The requirements of public speaking and peer judgment efficiently combined all my fears into one nice, giant ball of stress and anxiety. Nevertheless, I took all my worldly experience and decided to deliver a message about the things we take for granted and responsibility, topics that every 17-year-old is deeply well versed in. While I believed I delivered a powerful message, the B- received and the peer feedback of “preachy and lacking references to real data” may indicate otherwise.

I was recently reminded of those times when I was asked to write original content for our initial Newcleus newsletter, which has been met with a similar set of feelings and if I’m being honest, similar thoughts for potential content. I feel I can improve upon my original oratory topic as it comes with an additional 25 years of life (17 of them with Newcleus), recession(s), tax law changes, marriage, mortgage payments, home improvements, home equity line, future tuition payments, aging parents, two dogs, and pandemic…oh, and pandemic-era dog adoption, three dogs, how could I forget.

While we all may have faced similar challenges, experiences, and responsibilities, I think most of us would gladly take Speech class type fear over the real-life responsibilities that come with age. As Chief Operating Officer of Newcleus, I don’t mind taking another swing at this topic, albeit in the theatre of employer sponsor plans, done from the comfort of my office chair, and the absence of the always-so-fair social judgment of high schoolers, as I know the approach and strategies offered work. And, if done correctly, these approaches can turn these stressors into opportunities for both employers and employees.

I don’t know how others would describe me, but I doubt “sub-standard” is at the top of their list, at least from a life insurance underwriting perspective. I can tell you it’s at the top of mine, and, while my wife and doctor may add or elevate “idiot” to the top of their description list after hearing me say that, it is something I constantly think about, especially when coupled with all the aforementioned stressors. So, what do we do? Get the standard multi-million-dollar term life insurance policy upon certain life events? Sure, most do and should. But, if you have sub-standard concerns, smoke (even occasionally), or wait too long, even if it’s to get in better shape, your premiums will increase.

The ability to apply for life insurance is becoming more and more accessible. You probably have seen the “up to $2 million of coverage without medical exams”, which, for a country that has over 106 million underinsured adults and only 50% of adults reporting that they own life insurance is a good thing1. Personally, given my situation, I would approach this with apprehension, as I know my “without medical exams” will certainly lead to a prescription review, request for doctor’s exams, and review of my Medical Information Bureau report (“MIB”). If your credit report is for money lenders, your MIB report is for insurers and just like credit reports, your history, including results for previous underwriting results, even if not directly disclosed on your application, may impact your premiums and underwriting requirements. All of this to say, for me, the shine of those advertisements quickly wears off.

So now what? If you have insurance coverage concerns, even if in good health if you have an employee-sponsored group term plan, make sure you are properly taking advantage of your employer-sponsored programs. Why? Tax advantage and power in numbers.

Analysis

Generally speaking, if the plan is offered to everyone, and the paid-for employer-provided coverage exceeds $50,000, the employee is not taxed on the first $50,000 of coverage (meaning it’s free). The coverage that exceeds $50,000, maybe because you are entitled to a multiple of salary, tax is due on the economic benefit of the excess coverage. The amount of tax paid is based on rates published in IRS Publication 15b, and these rates are typically cheaper than retail, personal term insurance.

Next, if you can get more coverage through your employer’s voluntary life insurance program, over and above what the employer pays for, you may want to consider paying for more coverage. This is the power in-numbers benefit where due to the size of the group, the questions asked to obtain more coverage are typically less intrusive and quicker to implement than your typical term insurance application. The downside of most group term plans is the limited amount of coverage. You may be entitled to a multiple salary, but it also may be capped at $300,000. So, you may feel stuck as the employee, but if you are in a position where you are the employer or responsible for the employer-sponsored programs, there is a way to remove those caps, which can accommodate those that are hitting the cap or save money for those that may be paying premiums for personal coverage.

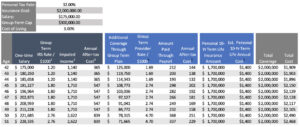

By way of example, let’s say your personal goal is to have $2 million of personal life insurance coverage and your employer has a group term plan that offers a one-time multiple salary benefit with a $300,000 cap. You’re 42 years old, have an insurance rating that would be considered standard non-tobacco, and a salary of $175,000. Your avenue and costs associated with obtaining coverage may look something like*:

The above example does not include any adjustment for the fact that the personal term insurance coverage is paid for with after-tax wages and rates will fluctuate based on your underwriting results and carrier used. Also, if you’ve been putting off the decision to obtain this coverage, the longer you wait, the more expensive they can become. In any event, there are more efficient ways for employers to assist employees with reaching these goals, which can also assist with employee retention efforts.

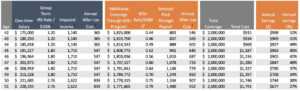

With 66.5% of Banks in the US and countless corporations owning Bank/Corporate-Owned Life Insurance (“BOLI”), there are other options to leverage this employer-owned life insurance to remove caps, reduce underwriting requirements, and reduce expenses for both the employer and employee. BOLI Programs also have a power-in-numbers dynamic where guaranteed issued coverage could be obtained on as little as five employees2; guaranteed issued is where the underwriting requirements are limited to few questions related to your time missed at work due to illness, smoker status, and consent to your employer obtaining this type of coverage. If BOLI was used in the above scenario, the impact on the employee may look something like this:

This approach doesn’t have to be implemented with a new purchase of BOLI. Existing programs can be modified to implement this strategy and it can also be used to carve into the one-time salary option to lower the employer’s cost associated with providing these types of programs and further reduce the impact on the employee. And, while it is true that BOLI coverage must be limited to the top 35% of the employee base, this sub-set of employees is usually where the need is the strongest.

With every program and approach, there are trade-offs and things to consider. For example, the BOLI solution may be tied to the employee’s employment status with the employer, meaning the employee may not be able to take this coverage with them. At the same time, the BOLI approach can extend beyond 10 years, including into retirement, where no future underwriting is required; unlike personal term coverage where rates may increase, or underwriting may need to be reassessed and/or the individual may need to reapply. The other thing to consider is whether this level of coverage is needed as life events pass, responsibilities are fulfilled, and risk diminishes, you become more “self-funded”, and your focus shifts towards retirement.

Regardless of your situation, this is a simple strategy that can become part of an employer’s overall employee retention strategy, a way to reduce costs, boast earnings, and find solutions to the challenges that face many employees today.

On deck for future newsletters, Newcleus will discuss ways to bridge the retirement income gap that may come for traditional qualified plans through the implementation of non-qualified plan solutions and reduce costs associated with those plans through 401(k) fee reduction and Pension plan de-risking. Please know that we are always working on these solutions and implementations, so if you don’t want to wait until the publication of those strategies and/or to obtain more information on any of the topics discussed, including Group Term Plan, Group Term Replacement/Carve-out Plans, Personal Term Insurance, Financial Planning, etc., please do not hesitate to contact me at rpearson@newcleus.com.

Disclaimers for Graphs:

* The information provided herein is based solely on our informal, general understanding of the relevant technical issues as well as the products and plans that may be involved. This information is not intended, nor should it be used as an opinion on legal, tax, or accounting matters. This material is for informational purposes only and does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any securities or other financial instruments. Clients are strongly urged to seek independent accounting, tax and/or legal counsel for advice in applying this information.

-

The IRS requires employers to report an amount includable in gross income that represents the economic benefit of coverage provided by the employer. Employers can generally exclude the cost of up to $50,000 of group-term life insurance coverage from the wages of an insured employee. The cost per $1,000 can be found in the IRS Publication 15-b: https://www.irs.gov/pub/irs-pdf/p15b.pdf

-

This is the amount that would be included in the insured employees’ wages.

-

Amount withheld and payable to the IRS, which is generally done via the employer’s payroll system. This calculation is based upon an assumed individual tax rate of 32%

-

Based upon Group Term Coverages through Principal Life

-

Based upon the average of five highly rated life insurers that offer 10-year term coverage.

REFERENCES:

-

Bankrate: https://www.bankrate.com/insurance/life-insurance/life-insurance-statistics/#:~:text=In%202022%2C%20106%20million%20American,owning%20life%20insurance%20in%202022

-

Coverage is offered through Protective Life’s BOLI and is subject to certain guidelines. Coverage is not guaranteed. This reference is for informational purposes only and does not constitute an offer to sell, a solicitation of an offer to buy, provide a guarantee of eligibility, or a recommendation for any securities or other financial instruments Please contact Newcleus for additional details and requirements.